Level: Easy

Goal: Classic monthly airline passenger series (trend + seasonality) using a library dataset.

Dataset & Library

- Dataset: AirPassengers dataset via

statsmodels.datasets.get_rdataset - Library: statsmodels

Installation

pip install statsmodels

Data Loading

import pandas as pd

from statsmodels.datasets import get_rdataset

data = get_rdataset("AirPassengers", "datasets").data

# Original data typically has a 'time' or 'Month' column and 'value' column

print(data.head())

# If there is only an index and a passenger column:

# Example conversion (adapt depending on structure)

data["Month"] = pd.date_range(start="1949-01-01", periods=len(data), freq="M")

data = data.set_index("Month").sort_index()

data.rename(columns={data.columns[0]: "Passengers"}, inplace=True)

print(data.head())

Implementation Steps

1. Data Loading and Exploration

- Load AirPassengers dataset using statsmodels

- Inspect data structure and format

- Convert to proper time series format (datetime index)

- Examine basic statistics and data range

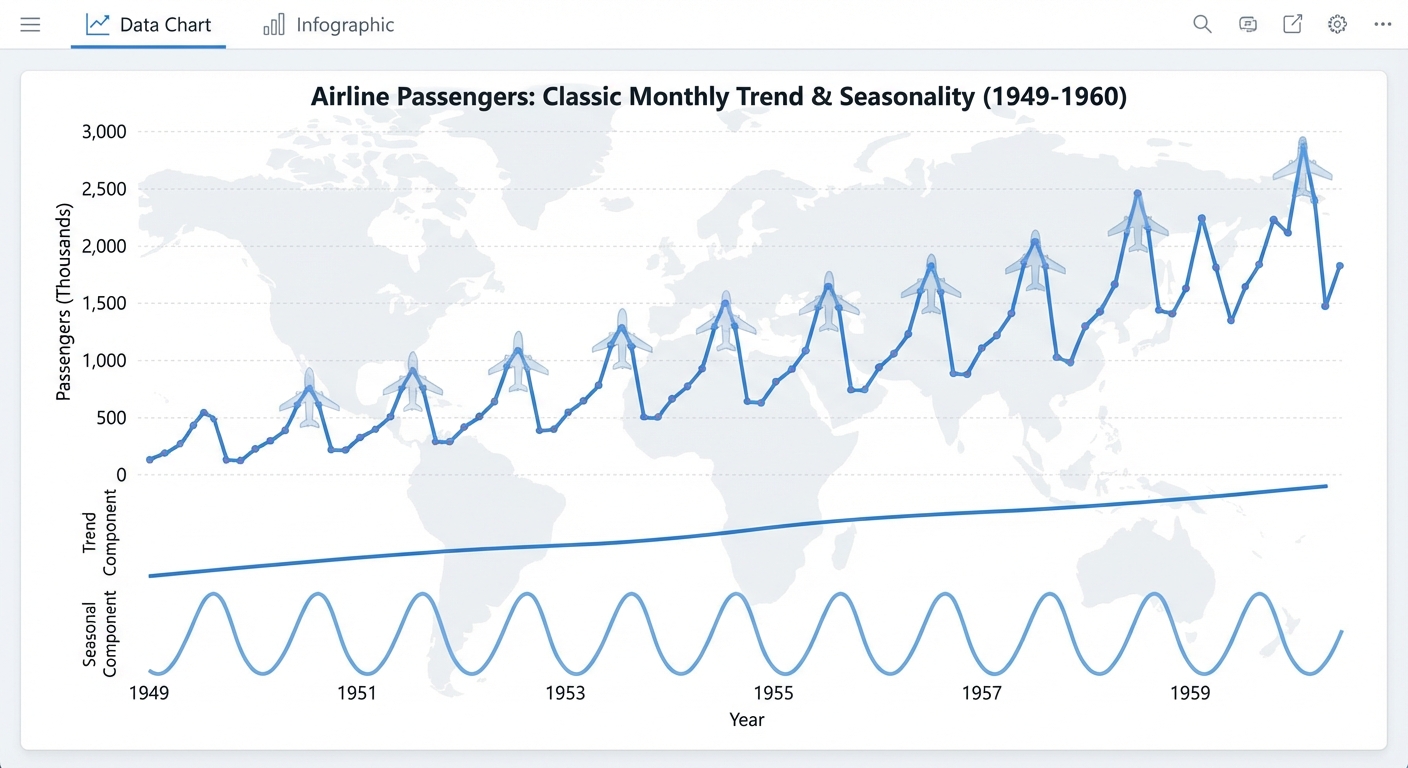

2. Exploratory Data Analysis (EDA)

- Plot the time series (should show clear trend and seasonality)

- Identify trend (increasing over time)

- Identify seasonality (yearly pattern, peak in summer)

- Perform time series decomposition (additive or multiplicative)

- Calculate and visualize ACF/PACF plots

3. Stationarity Analysis

- Test for stationarity (ADF test) - will be non-stationary

- Apply first differencing

- Apply seasonal differencing if needed

- Test transformed series for stationarity

4. Model Building

- ARIMA Models:

- Use ACF/PACF to identify (p, d, q)

- Try multiple ARIMA configurations

- SARIMA Models (recommended):

- Identify seasonal pattern (12 months)

- Fit SARIMA models: SARIMA(p, d, q)(P, D, Q)12

- Try different seasonal configurations

- Exponential Smoothing:

- Holt-Winters method (additive or multiplicative)

- Compare with ARIMA/SARIMA

5. Model Selection

- Compare models using AIC/BIC

- Use cross-validation or hold-out validation

- Select best model based on validation performance

- Check residual diagnostics

6. Model Evaluation

- Split data (e.g., last 2 years as test set)

- Generate forecasts

- Calculate accuracy metrics (MAE, RMSE, MAPE)

- Visualize forecasts with actual values

- Analyze forecast errors

7. Forecasting

- Generate future forecasts (e.g., next 12-24 months)

- Include prediction intervals

- Visualize with historical data

- Interpret results

Expected Deliverables

EDA Report:

- Time series plot showing trend and seasonality

- Decomposition plots (trend, seasonal, residual)

- ACF/PACF plots

- Stationarity test results

Model Results:

- Best model with parameters (e.g., SARIMA(1,1,1)(1,1,1)12)

- Model diagnostics (residual plots, ACF of residuals)

- Forecast accuracy metrics

- Forecast plots with confidence intervals

Code:

- Complete Python notebook

- Functions for model fitting and evaluation

- Visualization utilities

Tips

- This is a classic dataset perfect for learning ARIMA/SARIMA

- Strong seasonality (yearly pattern) - SARIMA is highly recommended

- Multiplicative seasonality is common (variance increases with level)

- Use seasonal differencing for SARIMA models

- Compare additive vs multiplicative models

- This dataset is well-studied - results should align with literature

- Good for demonstrating Box-Jenkins methodology

- Perfect for understanding trend + seasonality decomposition